Over the past few years, the fintech industry has been rapidly reshaped by accelerating technological innovation and evolving customer expectations.

At the heart of this transformation lies the rise of open banking and the API economy, which are redefining how financial services are built, connected, and delivered. By enabling seamless integration between banks, fintechs, and third-party platforms, APIs are not just improving efficiency, they’re fundamentally changing the financial ecosystem.

In this blog, we explore how API-driven collaboration is transforming fintech and reshaping the modern digital economy.

Open Banking empowers consumers with full control over their fiscal data, allowing them to decide who can access it, for what purpose, and for how long. This shift from institution- possessed data to user-authorized data introduces more transparency and trust into the fiscal system.

Traditionally, customers were limited to the products and services offered by their primary bank. Open banking solves this by enabling third-party providers (TPPs) to make tailored financial solutions.

For illustration, by assaying spending patterns, fintech platforms can recommend profitable product assortments, optimized credit cards, or intelligent savings plans aligned with individual fiscal behavior.

By granting secure access to financial insights, Open Banking APIs encourage competition, expand consumer choice, and accelerate the delivery of innovative financial products.

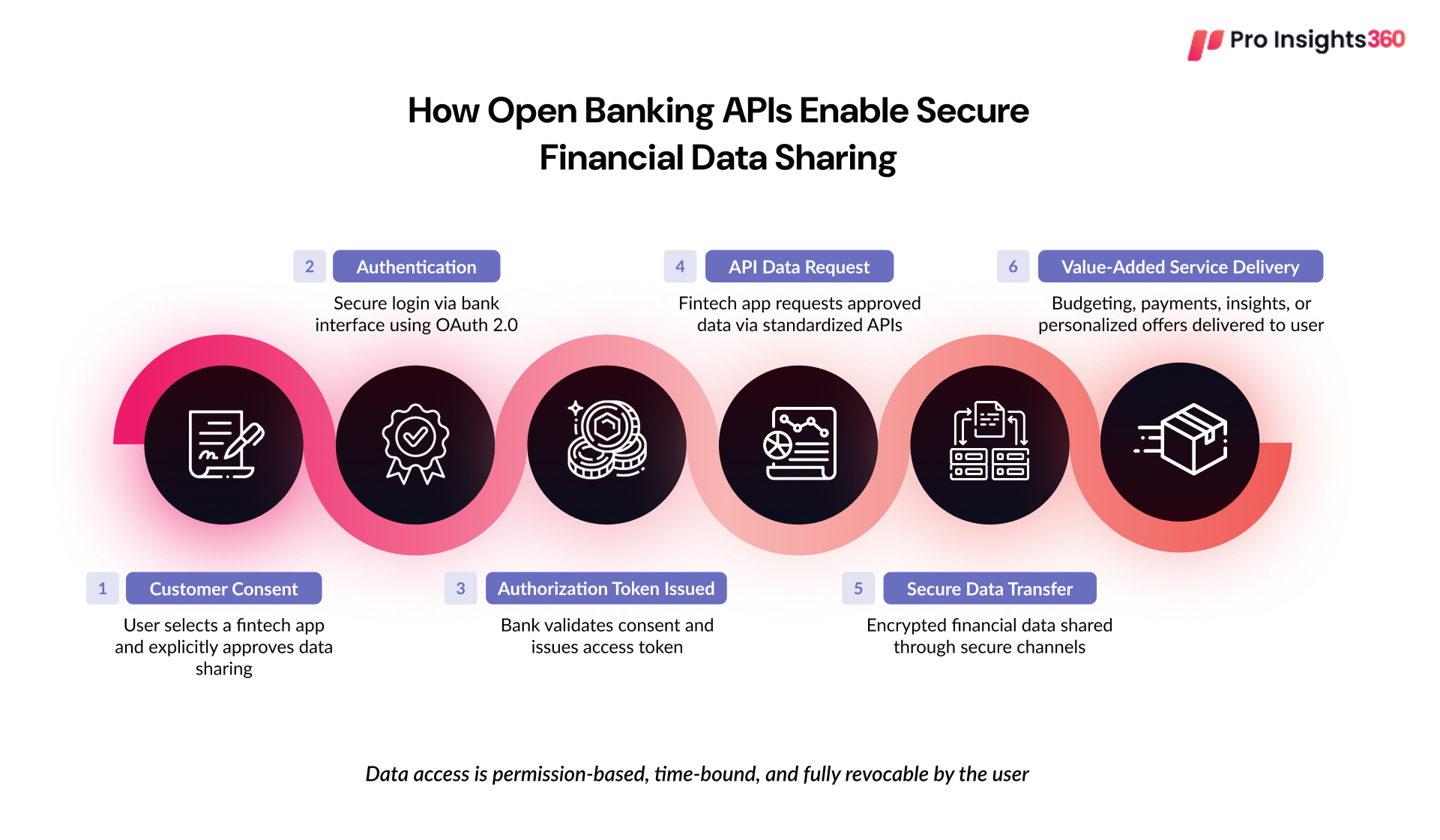

APIs enable consumers to grant third-party applications an access to data without hampering security by delivering safe and standardized record sharing, usually via OAuth 2.0 protocols.

Since open banking apps are developed with fortified authentication procedures, concrete security standards, and data encryption, end users can be rest assured of their information security.

Fintech institutions and banks can immediately scale their offerings and react to changes in customer demands due to APIs. All this without reconfiguring the entire system.

For instance, instead of opting for time-consuming and expensive process of building a similar service from scratch, a fintech institute can launch a new budgeting platform by collaborating with some third-party service through API.

Banks and third-party providers (TPPs) can exchange data through a standardized, safe channel due to APIs. This procedure assures that the exchange conforms with regulatory requirements and that only authorized parties can access logs. The open banking solutions function in the following way:

API and open banking use a general set of information formats and protocols throughout the fintech territory. Developers now can seamlessly create apps that can coordinate with multiple financial institutions without any need for altering the integration for each one.

A customer must grant permission prior to TPP accessing the client’s data. This usually takes place by integrating bank accounts and enabling TPP access to metrics through open authorization (OAuth) procedure.

TPPs can offer a range of services, including payment services, personalized financial advice, and financial output management tools, using the data they have obtained. For instance, a budgeting platform may leverage transaction insights to assess user’s expenses and detect pockets where they might save.

With permission, TPPs can access the bank’s servers via the APIs, obtaining information from the bank’s systems, including account balances and transaction history.

Robust open banking security mechanisms protect sensitive and critical financial data. Some of these precautions include secure coding patterns, encryption, and regular security audits. They protect client’s records and reduce the risk of data breaches.

Most components of the API economy collaborate to offer innovation, competitiveness, and teamwork to the world. They are:

The major factor that influences how core banking API executes is the set of regulations laid down by governments. These regulations mandate that banks share their data and services with outside developers while protecting individuals’ private information.

APIs are similar to flexible banking’s constituent elements. OAuth 2.0, RESTful APIs, and OpenID Connect are some of the examples of bank API integration standards.

It becomes imperative to set exclusive data governance standards to exchange economic insights in a responsible manner, adhering to security compliance requirements.

The segments under this exercise are consent coordination, transparent transactions, maintaining the records amassed, ensuring precision, and data utility accountability.

When discussing Open Banking and the API economy, the potential for growth and innovation is undeniable. But so are the challenges that must be addressed, including.

Financial institutions face the delicate issue of protecting sensitive customer data, by investing in robust security to cut back on the threat of data breaches and protect consumer confidentiality.

Compliance to changing and at times intricate regulatory guidelines also pose a challenge, which financial institutions meet with non-stop scrutiny and strict operating procedures.

The construction, integration and scaling up of APIs can be an intensive process that demands specialized skills and is a huge time investment.

To get on top of these hurdles, banks and third-party providers need to work together to set up and agree upon industry standards, throw more money into cybersecurity and put the customer’s interests at the forefront of their Open Banking plans.

Open banking is revolutionizing financial services by delivering accessible, transparent, and tailored product experiences.

Through APIs, banks and fintech institutions can deliver latest services that facilitate users to maintain financial data, coordinate multiple accounts, and get more insights into their financial well-being. This entirely functions on secure and user-friendly platforms.

For enterprises, the API economy serves trending opportunities to extend services and collaborate across different verticals. By adopting Open Banking APIs, businesses can create unified, user-centric solutions that exceed traditional banking dynamics and penetrate smart wealth management and insurance. This altogether drives variety, innovation, and long-retained user trust.